A rollover is the movement of funds from one retirement savings vehicle to another. You may want to make a rollover for any number of reasons — your employment situation has changed, you want to switch investments, or you've received death benefits from your spouse's retirement plan.

There are two possible ways that retirement funds can be rolled over — the indirect (60-day) rollover and the direct rollover (or trustee-to-trustee transfer).

The indirect, or 60-day, rollover

With this method, you actually receive a distribution from your retirement plan and then, to complete the transaction, you deposit the funds into the new retirement plan account or IRA. You can make a rollover at any age, but there are specific rules that must be followed. Most importantly, you must generally complete the rollover within 60 days of the date the funds are paid from the distributing plan.

If properly completed, rollovers aren't subject to income tax. But if you fail to complete the rollover or miss the 60-day deadline, all or part of your distribution may be taxed, and subject to a 10% early distribution penalty (unless you're age 59½ or another exception applies).

Further, if you receive a distribution from an employer retirement plan, your employer must withhold 20% of the payment for taxes. This means that if you want to roll over the entire distribution amount (and avoid taxes and possible penalties on the amount withheld), you'll need to come up with that extra 20% from other funds. You'll be able to recover the withheld amount when you file your tax return.

The direct rollover, or trustee-to-trustee transfer

The second type of rollover transaction occurs directly between the trustee or custodian of your old retirement plan, and the trustee or custodian of your new plan or IRA. You never actually receive the funds or have control of them, so a trustee-to-trustee transfer is not treated as a distribution. Direct rollovers avoid both the danger of missing the 60-day deadline and the 20% withholding problem.

If you stand to receive a distribution from your employer's plan that's eligible for rollover, your employer must give you the option of making a direct rollover to another employer plan or IRA.

A trustee-to-trustee transfer is generally the most efficient way to move retirement funds. Taking a distribution yourself and rolling it over may make sense only if you need to use the funds temporarily, and are certain you can roll over the full amount within 60 days.

Should you consider a rollover?

In general, if your vested balance is more than $5,000, you can keep your money in an employer's plan at least until you reach the plan's normal retirement age (typically age 65). But if you terminate employment before then, should you consider a rollover to either an IRA or a new employer's plan? There are pros and cons to each move.

IRA: In contrast to an employer plan, where investment options are typically limited to those selected by the employer, the universe of IRA investments is almost unlimited. Similarly, the distribution options in an IRA (especially for your beneficiary following your death) may be more flexible than the options available in your employer's plan.

New employer's plan: On the other hand, employer-sponsored plans may offer better creditor protection. In general, federal law protects IRA assets up to $1,362,800 (scheduled to increase on April 1, 2022) — plus any amount rolled over from a qualified employer plan or 403(b) plan — if bankruptcy is declared.* (The laws in your state may provide additional protection.) In contrast, assets in a qualified employer plan or 403(b) plan generally receive unlimited protection from creditors under federal law, regardless of whether bankruptcy is declared.

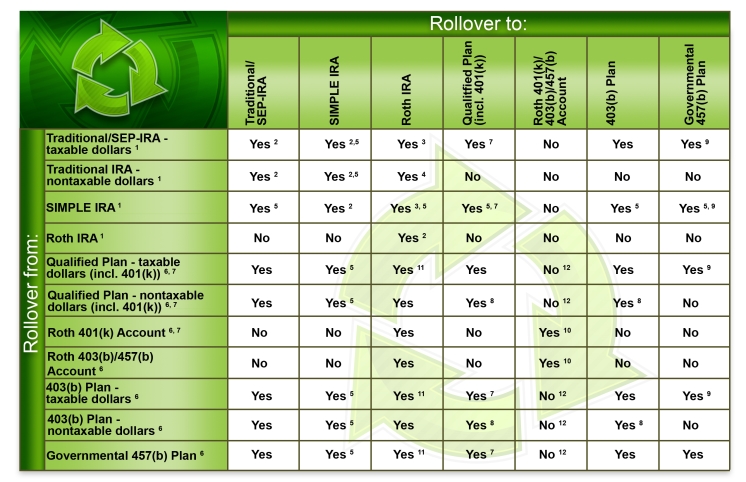

Use this rollover guide to help you decide where you can move your retirement dollars. A financial professional can also help you navigate the rollover waters. Keep in mind that employer plans are not legally required to accept rollovers. Review your plan document.

Some distributions can't be rolled over, including:

- Required minimum distributions

- Certain annuity or installment payments

- Hardship withdrawals

- Corrective distributions of excess contributions and deferrals

In addition to rolling over the assets to an IRA or new employer's plan, or leaving the money in your current employer plan, you may also choose to take a lump-sum cash distribution. However, keep in mind that the distribution will be subject to income taxes and, if you're younger than 59½, a 10% penalty tax, unless an exception applies.

1 Required distributions and nonspousal death benefits can't be rolled over.

2 In general, you can make only one tax-free, 60-day, rollover from one IRA to another IRA in any 12-month period no matter how many IRAs (traditional, Roth, SEP, and SIMPLE) you own. This does not apply to direct (trustee-to-trustee) transfers, or Roth IRA conversions.

3 Taxable conversion

4 Nontaxable conversion

5 Only after employee has participated in SIMPLE IRA plan for two years.

6 Required distributions, certain periodic payments, hardship distributions, corrective distributions, and certain other payments cannot be rolled over; nonspousal death benefits can be rolled over only to an inherited IRA, and only in a direct rollover.

7 May result in loss of qualified plan lump-sum averaging and capital gain treatment.

8 Direct (trustee-to-trustee) rollover only; receiving plan must separately account for the after-tax contributions and earnings.

9 457(b) plan must separately account for rollover —10% penalty on payout may apply.

10 Nontaxable dollars may be transferred only in a direct (trustee-to-trustee) rollover.

11 Taxable dollars included in income in the year rolled over.

12 401(k), 403(b), and 457(b) plans can also allow participants to directly transfer non-Roth funds to a Roth account if certain requirements are met (taxable conversion).

*Non-deposit investment products and services are offered through CUSO Financial Services, L.P. (“CFS”), a registered broker-dealer (Member FINRA / SIPC) and SEC Registered Investment Advisor. Products offered through CFS: are not NCUA/NCUSIF or otherwise federally insured, are not guarantees or obligations of the credit union, and may involve investment risk including possible loss of principal. Investment Representatives are registered through CFS. The Credit Union has contracted with CFS to make non-deposit investment products and services available to credit union members.

Financial Advisors are registered to conduct securities business and licensed to conduct insurance business in limited states. Response to, or contact with, residents of other states will be made only upon compliance with applicable licensing and registration requirements. The information in this website is for U.S. residents only and does not constitute an offer to sell, or a solicitation of an offer to purchase brokerage services to persons outside of the United States.

CFS representatives do not provide tax or legal guidance. For such guidance please consult with a qualified professional. Information shown is for general illustration purposes and does not predict or depict the performance of any investment or strategy. Past performance does not guarantee future results.

Copyright 2021 Broadridge Investor Communication Solutions, Inc. All rights reserved.